You have options

Knowing your money

To know your money, it’s important that you understand the RISK that your money has. The choices you have available to you during retirement planning age have a lasting impact. That’s why we want to be transparent with you. The current economy is very different than it was 15 years ago. For example, things we see people utilizing every day are Stocks, Bonds, Mutual-Funds, Variable Annuities, Money-Market Accounts, and so forth. We believe you need to learn the truth about these before you decide to make use of them.

A good retirement plan should out-last you, and continue on contributing to your loved ones.

Stocks, Bonds and Mutual Funds

Stocks, Bonds and Mutual-Funds are quite popular for retirement planning. Why wouldn’t they be? We have been in one of the longest bull-runs in history! Why would you want to miss out on an average of 21% year-over-year ROI?

All bull-runs end. There is a looming risk of a major market correction.

Stocks, Bonds and Mutual-Funds carry fees along with considerable risk in today’s market.

Carrying a large portion of your money in Stocks, Bonds and Mutual-Funds is not a safe option anymore.

Variable Annuities

Variable Annuities are a popular retirement option because they offer tax-deferred growth on gains. You only begin paying taxes upon withdrawal or receiving a monthly income from the account.

Variable Annuities carry EXTREMELY high hidden-fees over time.

By the time it’s over, you’ll have paid enough in fees to have opened and funded an entirely new retirement account. Instead of your money staying with you, it’s gone someone else’s pocket.

CD's, Money-Market and Savings

CD’s, Savings and Money-Market seem like a very viable and safe option for a long-term retirement plan.

The average percentage rate for these is incredibly low, below 1% is common.

Now an interest of around 1% might not sound awful, and you have the power of compounding interest on your side!

However, when you consider the fact that the U.S has an inflation rate of 7.9% According to The Bureau of Labor Statistics as of February 2022, your money will be disappearing without you even knowing. *1

The Risk According to FINRA

To better your understanding of the risks you take on by placing your retirement into the options above, let’s look at some quotes directly from The Financial Industry Regulatory Authority, FINRA.

- “While historic averages over long periods can guide decision-making about risk, it can be difficult to predict (and impossible to know) whether, given your specific circumstances and with your particular goals and needs, the historical averages will play in your favor. Even if you hold a broad, diversified portfolio of stocks such as the S&P 500 for an extended period of time, there is no guarantee that they will earn a rate of return equal to the long-term historical average.”

- “When it comes to risk, here’s a reality check: All investments carry some degree of risk. Stocks, bonds, mutual funds and exchange-traded funds can lose value, even all their value, if market conditions sour. Even conservative, insured investments, such as certificates of deposit (CDs) issued by a bank or credit union, come with inflation risk. They may not earn enough over time to keep pace with the increasing cost of living.”

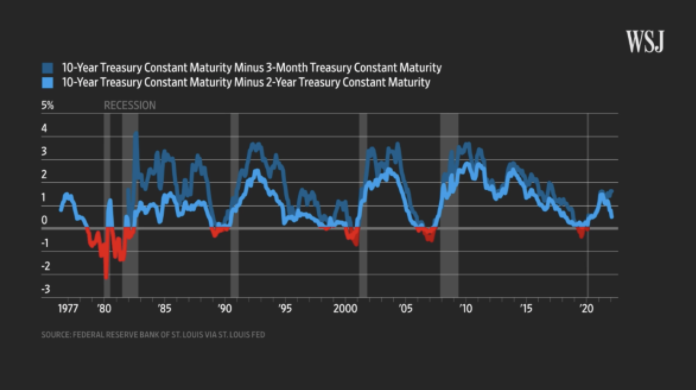

"The Inverted Yield Curve"

From the WallStreet Journal:

- “When short-term interest rates are higher than long-term interest rates, a phenomenon Wall Street mavens call an inverted yield curve, it is sometimes a signal of recession.”

This happened in the U.S in March 2022.

Information is the key to success. If you aren’t convinced, or disagree with the points made above about some of the most common retirement strategies, we strongly urge you to take a long look at what’s been happening in the greater global economy. Knowing your money means that you know your money’s RISK.

The market is getting increasingly complex, but your retirement doesn’t need to be, as well.

Please call us at 859-967-4663 if you need help planning yours, or just want to talk about your current plan.